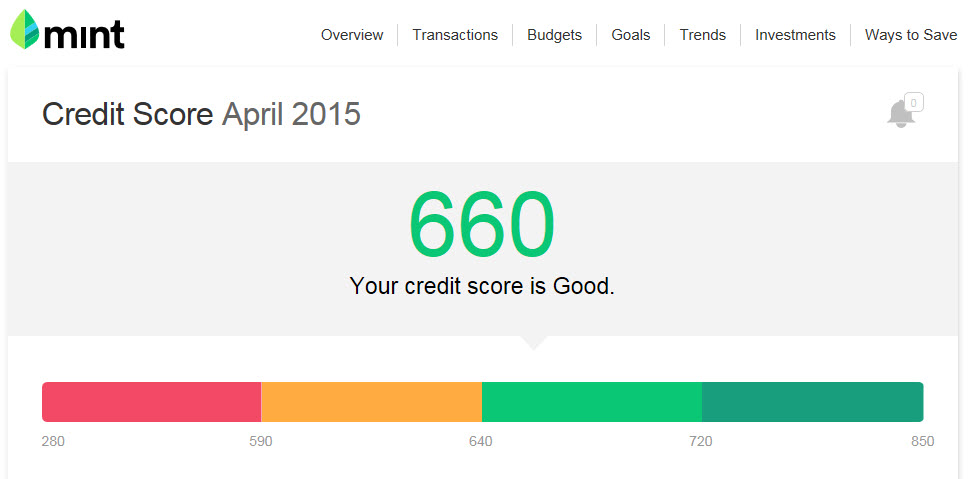

660 Credit Score

What credit can I get with a 600 Credit Score?

I need a cosigner with a 660 or better credit score and a decent credit history to secure my business loan.

The ‘bar’ has been raised to 660 for ‘Prime”??? Used to be 620 was the considered the lowest credit score for prime which was still considered good. Now 660 is considered only good but not great credit.. Why does one have to do FHA with a 615?? why not the 2.875% deal?

Grant provides up to 4% of a loan’s value

Home is Possible grant program helps make the dream of home ownership a reality for qualified Nevadans. Focused on homebuyers in Washoe and Clark Counties, the grant provides up to 4% of a loan’s value for down payment and closing costs. The grant never needs to be repaid. Program Requirements Minimum credit score of 640 for government insured loans, 660 for manufactured homes and 680 for most conventional loans Qualifying income on mortgage application must be below $95,500 Home price below $400,000 Homebuyer education course required Must meet normal government or conventional loan underwriting requirements http:// housing.nv.gov/programs/FTH/Home_is_Possible/

Your tax dollars

Helping Nevadans Feel at Home Home is Possible grant program helps make the dream of home ownership a reality for qualified Nevadans. Focused on homebuyers in Washoe and Clark Counties, the grant provides up to 4% of a loan’s value for down payment and closing costs. The grant never needs to be repaid. Program Requirements Minimum credit score of 640 for government insured loans, 660 for manufactured homes and 680 for most conventional loans Qualifying income on mortgage application must be below $95,500 Home price below $400,000 Homebuyer education course required Must meet normal government or conventional loan underwriting requirements http:// housing.nv.gov/programs/FTH/Home_is_Possible/

A Question about Old Debt

I have about 7K in old Credit Card debt that I stopped paying on about 5 years ago. I started to get collection letters again. My score is fairly low, 660, and this is probably why. I have the money to pay it all off, my question are as follows: 1. Do I pay off the full amount and be done with it. If I do this will it help my credit score. 2. Do I pay off a settlement amount which is about %50 of the actual amount, 3500. If I do this will it be worse for my credit. 3. Do I just do nothing. I don’t need my credit for anything. I have owned my house for 10 years now. I have a fairly new car and 2 other credit cards with zero balances. Any insight is helpful. Debating on going to a mortgage broker to see what they think. I plan on moving maybe in 5 years or so. So wondering if it makes sense to be done with it now.

fico score

I’m having problems with my credit. I had a 805 credit score last year. I had a loan forgiven. I never missed a payment. Transuion reports it as no neg history, and “paid as agreed”. Somehow FICO is interpreting this as a “serious delinquency”. They dropped my score to 660. I disputed the entry with Transuion, but there is nothing to dispute since it is accurate. You can’t dispute FICOs wrong interpretation. I call the 1800 number, and get lectured about how to protect my credit. I call the lenders who turn me down, and they say call transunion. I call transunion, and they say call the lender. what a runaround mess.

Unsecured/No Collateral Loans Up Tp $200,000 < AlternativeFunding

I’ve researched several funding programs, and this is the BEST that I have seen. It’s a Credit Line, not a Loan, so you don’t have to pay it off by a deadline. This program will improve your credit, not hurt it. Additional funding is made available to you after a successful payment history. I have developed personal relationships with the larger banking institutions and they are giving me their “turn-downs” and I am able to get their clients the funding needed. Nobody can compete with this program. Whether you are a start-up or you’ve been in business for years and need working capital, we can help! Get Funding Now… Get Up To $200,000 For Your Business Fast 24-Hour Approvals, 2-Week Funding 0% Introductory Interest Rate Specials for 6-12 Months (As Low as 7% APR thereafter) Start-ups Welcome; No Business History Needed Free Legal and Small Business Consulting Included 660 Min Credit Score — Bad Credit? Credit Partners Accepted! Absolutely No Upfront Fees Required! No Financials Needed — No Collateral Needed No pre-payment penalties We also have a Law Firm that will structure your retirement to avoid penalties and additional taxes, in addition to structuring enity for start-ups. In the last 10 years, we’ve helped thousands of people just like you. During 2011, we raised over $30 Million for business owners all across the United States. If you need funding, we can help. Contact us today and we will assign a funding specialist who will work closely with you to facilitate your individual needs and get you fast funding and build your credit in addition to giving you a free analysis and explanation of what options exist for you. Paradigm Shift for betterment of humankind…making money make a difference…

Is a 660 Credit Score the new 600??

The dividing line between prime & subprime used to be 600, now it is 660?? How many chargeoffs are you allowed before you are considered to have bad credit?

Ha I foreclosed and my credit score sky rocketed

too funny The late payments on open debt brought it down to mid 500’s….now it is at 660…. I have a 5% Debt to income ratio Time to go finance a new car.

Is a Credit Score of Under 660 Subprime?Really?

I thought the cutoff was between 580-620… 660 is considered good credit and anything under 598 is considered needs improvement?? Banks issued 5.4 million new credit cards to subprime borrowers through June, up 64% from a year earlier, according to the most recent data from credit bureau Equifax. The company defines a subprime borrower as having an origination risk score–a proprietary definition–of less than 660.

Banks are Lending Again, Get Approved Now!!!

We provide consumers (and Mortgage Bankers & Brokers) the most efficient and cost-effective method of obtaining a mortgage that fits the consumer’s financial goals and circumstances. We can help many consumers, including low-to-moderate income borrowers with worse than BAD CREDIT and/or BANKRUPTCIES. We can APPROVE Mortgages for Buyers with Bad Credit (including Bankruptcies). Note: We APPROVE loans if your Credit Score (FICO) is BELOW 500, if you have a Co-Borrower with a Credit Score of 550+ via some of our LENDERS! PRIVATE LENDERS (8 Day Closings Available) $ = EQUITY LOANS (w/ 8 Day Closing) – $50,000-$250,000 [660] $ = BUSINESS-Equity/CREDIT LINE (Minimum: 1 Year in Business): $ 50,000+ to $100,000 (3 Days to Close) $100,000+ to $250,000 (3+? Days to Close)Need 660 credit score to ask for $ there

I don’t understand why Experian will tell me

“You’ve got good credit and your score is 701” whereas TransUnion tells me, “You’ve got crappy credit. Your grade is D, and your score is 660.” What gives? Anyone know?

Who’s got the best Auto Financing ?

Wells Frago, my bank, was in the upper atmosphere, checked a credit union, and they were better, at 9%, but still not so great. Looking to borrow $10K with a 660 score for 60 months. Where are the best deals ?

Credit score

Does anyone know… if your credit score has dropped to 660 from 750, how long after consistently on time payments, no inquiries, and no additions to balances, the score would take to climb back up?

What is realistic min score to get business line

I am trying to figure out what the “norm” minimum FICO score is to pull a business line of credit right now in CA. Last year, my banker told me 650; now he’s saying absolute min 680. Just curious…Has anyone out there given/received a business line of credit lately for a score of 660? That is, with the financials being good besides that? If so, can you point me to a website/company? Thanks!

When you are given a monthly “mortgage” payment amount, does that refer to the total amount AFTER things like insurance, interest, etc. is factored in or are those things additional monthly expenses ON TOP OF the “monthly mortgage payment”?

Usually that refers to mortgage, property tax, and insurance. The second two are prorated over twelve months in “escrow” so the mortgage services can make interest on it. If you are lucky you might be able to get out escrow and pay these in lump sums on their annual due dates yourself. You might also figure in fairly fixed costs like utilities, maintenance, and enighborhood association fees. In some locations with high property tax and utilities the mortgage coudl be as little as half of your monthly housing cost.

How good of a credit score (I am actually looking for a number or range of numbers here…not the “good”/”fair”/”poor” ratings) do you have to have to get a loan from a local bank?

Until recently you had to be breathing, and even that was over-qualified. “For example, here’s what a borrower could have expected to be charged in interest for a $300,000 30-year fixed rate mortgage, based on his credit score, according to interest rates: How FICO score affects mortgage rates 760 to 850 tier 5.780% 700-759 tier 6.002% 660-699 tier 6.286% 620-659 tier 7.096% 580-619 tier 8.583% 500-579 tier 9.494%.” In what ways does a home loan (and I am assuming this is the same thing as the “mortgage”??) from a local bank differ from one from a “mortgage company”? Banks may have a a little better prices. You are allowed to shop around. There are mortgage brokers who shop for you – they colelct a fee from the eventual lender. Mortgages are often resold among companies, so you may be paying someone different by the second year. No change in price.

On FICO credit scores

Since lots of questions are posted here about credit scores, I thought I’d post a few exerpts from an article I recently read that might be of interest. It looks like there have been some changes (and a few things that may be worth re-mentioning)… On FICO credit scores… “Until this summer’s subprime crisis, a score of 720 or higher earned you some of the best interest rates, says John Ventura, director of the Texas Consumer Complaint Cetner at the University of Houston Law School. Borrowers now need a score in the high 700s to get the same benefits, he says.” “Getting the best rates could save thousands of dollars…if consumers with an average score increased their score by only 30 points, they would save $76/year in finance charges.” Regarding mortgages & credit scores: “The benefits are dramatic for mortgages. Raising a score from a range of 580-619 to 660-699 could save someone with a 30-year, $300K fixed mortgage, $5,148 in one year, according to myfico.com” “Consumers shouldn’t close old cards that they don’t use, because ‘closing an account eliminates a positive reference’ says Stephen Katz, a spokeman for TransUnion

credit scores

I had 30k in cc debt and my credit score was 690. I paid off my credit cards-all and one installment loan. My credit dropped to 660.reason given: because my balances are too high. Does anyone know why this happend?

Maxing your credit card out and paying balance-down

over two or three months looks responsible. Shows you know how to handle your money. Most credit cards only report once a month, so unless you need to get your credit pulled right away it doesn’t matter. If you want the card to report a certain balance for the month, pay it down to what you want before the statement close date. Most CC companies will report the closing balance through the entire month. Cap one indeed is starting to report limits. You will not have a 700 fico in 6 months if this is your first credit card ever. 6 months after I got mine I was in the low 600’s, 10 months later now I am 660-680. It will take you 6 months before you will even have a fico score. remember, just because you have a score does not mean you will get approved for credit. You will keep getting dinged for limited credit history. Cap 1 is a great “starter” card, so long as it does not have an annual fee. “Student” type cards are designed for those that have little or no credit history. Give it about 4 months and you will see lots of pre-approved offers for cards and loans. Finally, good intermediate places to get cards are: WAMU/providian (I got a 6K limit, 0% APR card from them) and HSBC (2% cash back). Gas cards are easy to get also, as well as department store cards like Macy’s. Dont bother applying for Amerian Express, Citi or Chase cards for a long time, they will just shoot you down.

more inquiries mean lower scores

At this point with a 630 you are pretty much stuck. I would try disputing some items on your credit report and trying to raise your score to at least 660. Your other alternative is to get a prosper loan and consolidate that way.

credit score and new loan

I’ve been disputing a hospital bill for 3 years now. Even though the charge is incorrect, I’ve been thinking about just paying it ($300). If the collection agency were actually to remove that mark, it might increase my credit score enough to more than pay me that amount back over the course of a loan. Is there anyway to ensure that a collections agency would inform credit agencies that debt has been paid? My other oncern is a great deal of credit card debt. This is all “arbitraging” 0%-started when stock oprtion trading at my company was halted by SEC, I was using that and employee stock purchase plan as major factor in budget. There is no credit card debt beyond 30 days-no balances but there have been quite a few opened in the past 18 months. Asdide from those 2 items, i have no dings on score. Those things alone lower it to 660. Any help would be appreciated.

Question about terminated phone service

I moved out of my apartment and let the past due balance on my MCI land line phone lapse and the account finally got terminated. Out of a past due amount of over $300, maybe one payment of $27 was made in February. Obviously the next step is collections When it does goto collections, 1) How long will it be until it gets reported to the credit bureaus. I plan on buying a house in the next few months and need to keep FICO score above 660. 2) How can I dispute this item to get it off the credit report. I hear that anything true or not can be disputed and must be deleted if can’t be verified within 30 days (true or not).

First dispute it online with one bureau then if you get a rejection, try convincing the collections manager the accounts are with that you moved a few times, and contacted the companies, but never got the new bills, etc… get a copy of their letter stating they will request the bureaus delete it, send that copy to the bureau as an appeal of the first rejection. I found that it was easier to convince the collection company who reported to the bureau that I was not given a fair chance to pay the bill, that the bill was BS in the first place, it was duplicate, wrong address, than it was to convince the bureau. I got 3 collections off of my credit and my score went from a 660 to a 771-799 and just bought a house with perfect credit. Email me if you have any questions, I am happy to help with advice to your situation perosnally. Be prepared because it took me almost 3 years to get this stuff cleared.

Repairing Credit? < credit-expert

Rebuilding your credit profile is going to depend on your starting credit score and what score you’d like to attain. A good target score is 660 or above. However, if you’d like more specifics you could provide additional details and I’ll be more than happy to provide some feedback on what your present actions are going to do for you as well as any future steps to take.

A quick fix

One of your other responders already mentioned this but I thought I’d corroborate it. One way to establish credit quickly is to talk with someone you know and trust (and vice versa), who also has a good credit score and ask them to add you to one of their credit card accounts as an authorized user. You won’t actually get to use your benefactor’s card itself but their credit rating will be yours in about a month. This maneuver will not adversely affect their credit, but it will bring yours up to speed. Some credit accounts report to only one credit bureau. Some report to all three major bureaus. If you can fanagle it, ask your friend/family member to sign you on to an account that reports to all three bureaus, so you will have all three scores that many lenders require. They’ll have to call their creditors to find out who they report to. This should be a temporary measure. Use your new piggy back credit rating to begin establishing you own good credit. Take out a merchant card and a competitively priced credit card and make your payments. Give your tradelines about a year to build and generate a solid history for you and then your benefactor can remove you. In the meantime, you can use your borrowed credit score to start shopping for a house. For maximum credit building effect, keep your new credit balances at about thirty percent of your credit limit. This shows the creditors that they can make interest money off of you, but not be too high of a risk. One of my housemates put this to work and brought two of my other housemates on to his credit card as authorized users. His tradelines became theirs and their credit improved dramatically. Parents do this with their kids frequently to get their credit established. I am a mortgage broker and I got these helpful tips above from a customer assistance employee at a credit reporting firm that my company uses. There are also home loan programs that are 100%. If you spend less than you make and have a minimum mid-FICO credit score of 660 you can also qualify for one particular loan that can literally pay off a home in five to ten years with no change to spending habits. My supervisors at work used it for their home and they are on track to pay off their $300,000 home in four to five years. Hope this helps.

660 seems to be popularly regarded

as good. Consider these quotes: “Nelson said his FICO credit scores are in the high 600s and low 700s, just below the cutoffs most lenders use for people with excellent credit”. -from ‘Why Going Broke is a Fact of Life in America’, by Liz Pulliam Weston, MSN Special Report (article), 6/30/2004 “The market is certainly substantial. By 2003, nearly 30 million American households either had no credit score — because they don’t use credit — or had a credit score below 660, the usual cutoff for “prime” borrowers. That’s according to CardWeb.com, one of the leading trackers of credit card trends.” -Same citation as just above “Don’t worry too much about your score of 700 or higher, Bodnar said. You’re already qualifying for lenders’ best rates.” -“I tell people not to be obsessive about it ,” she added. “Keep it in perspective: This isn’t the SATs. It’s not like you have to have a perfect 800.” -by Marshall Leob, in article titled “Financial Behavior Can Improve Credit”, 9/24/04, CBS Marketwatch.com “The three-digit credit score, which typically ranges from 300-850 is the most widely used measure of a person’a credit risk. Consumers with higher scores – the current U.S. average is roughly 723 – have an easier time securing low interest loans and other favorable terms on credit.” -can’t recall the source for this quote, but I copied it directly recently.

Quotes as possible guidance

“Nelson said his FICO credit scores are in the high 600s and low 700s, just below the cutoffs most lenders use for people with excellent credit.” -from “Why Going Broke is a Fact of Life in America”, by Liz Pulliam Weston, MSN Special Report (article), “The market is certainly substantial. By 2003, nearly 30 million American households either had no credit score — because they don’t use credit –or had a credit score below 660, the usual cutoff for “prime” borrowers. That’s according to CardWeb.com, one of the leading trackers of credit card trends.” -Same citation as just above “Don’t worry too much about your score of 700 or higher, Bodnar said. You’re already qualifying for lenders’ best rates. -“I tell people not to be obsessive about it ,” she added. “Keep it in perspective: This isn’t the SATs. It’s not like you have to have a perfect 800.”

question about improving overall credit score

This may be too simplistic a question but which is better: to pay down a $7000 installment loan quickly at a 26.99% fixed interest rate? or to pay down $2000 in revolving credit with a 18% interest rate? I know it may seem obvious given the interest rates, but I know that having too many revolving accounts counts against you too. I’ve paid down and closed 4 revolving accounts in the last few months and my score has gone up into the mid-600’s, like on average, between the 3 agencies, my score is about 650, 660. I only have so much savings left and I want to be smart about which to pay down first. I didn’t do enough research on the interest rate and I needed the money for medical bills so I’m stuck with it. I want to leave myself with one credit card, my student loans, and my car loan, and that’s it.