What Is a Credit Report

You balance your checkbook and check your portfolio, but how frequently do you check your credit files?

Credit files are windows into your private life. Lenders look at your credit history to assess your creditworthiness. It's to your advantage to know what your credit report says before you apply for credit so you can correct any inaccurate data. It can take up to six months for credit reporting agencies to make a change in your credit report, so give yourself at least that long before you start shopping for a mortgage, car or any other large purchase.

It's also important for you to understand that with the rise in identity theft and credit card fraud, you may not know that someone has assumed your identity or opened new accounts until they default on loans, or collection agencies start calling you. With a credit monitoring service like Identity Guard® CreditProtect, you will be notified of changes so you can act quickly if you suspect fraud.

What should I look for in my credit report?

It is important to frequently review your credit file to verify the following:

- Name

- Address

- Social Security Number

- Date of Birth

- All accounts listed are your own

- Credit/charge accounts

- Outstanding balances/limits on the accounts

- Payment histories

- Derogatory credit information has been deleted after seven years (non Chapter 13 bankruptcies after 10 years).

- Inquiries

Why should I review my credit files from all three credit reporting agencies?

Each credit reporting agency records information it receives from your creditors. You can't control which credit reporting agency (Equifax®, Experian® or TransUnionSM) your lender uses, so prepare yourself by checking all three agencies for accuracy.

What is a credit score?

A credit score is based on variables in your credit file that help determine your creditworthiness. The number is based on various factors, including the number of trade lines you have open, the number of late payments, delinquencies, etc. Lenders look at your credit file and other factors to determine your creditworthiness.

Your credit score is the product of a complicated formula, made up of several different elements that provides a measure of your creditworthiness. The higher your credit score, the less risk you present to a lender and, therefore, the more likely they are to let you borrow larger amounts, at better interest rates.

The most commonly used credit scores are those provided by Fair Isaac Corporation, called FICO® scores. A FICO score can range from 300 to 850.

Fair Isaac provides FICO scores to all 3 of the major credit reporting agencies: Equifax, Experian, and TransUnion. Each agency then adjusts the score based on the specific information it has for you. That means you actually have 3 different FICO scores, although they usually don't vary too greatly.

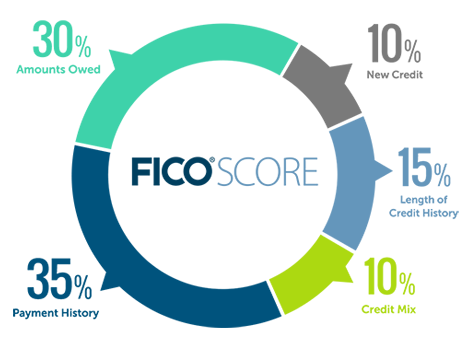

Your credit score is based on several factors, including:

|

Payment history. Your timeliness in paying all credit/debt accounts. Punctuality counts towards a higher score. Points off for past due or delinquent accounts, bankruptcies, and liens Total amount you owe. The ratio of your available credit to your total amount owed. Length of credit history. This segment also factors in the time since the last activity on each account. New credit accounts and inquiries. This includes the number of accounts you've 10% recently opened, as well as recent inquiries and any efforts to reestablish good credit. Types of credit in use. Based on the number of your accounts that are credit cards, installment loans, mortgages, etc. |

Why is my credit score so important?

Lenders carefully consider your credit score because it provides them with an objective measure of your creditworthiness. Your score can be impacted by many factors such as late payments, delinquencies, or high amounts of debt. Lenders may deny your loan or charge you a high interest rate if you have a low score. If you have a good credit history, you may have more options available to you resulting in lower interest rates and big savings.

Lower loan rates can mean thousands of dollars in your pocket over the years. If you purchase a home for $250,000 at 8.3% interest you will pay $679,306 over the course of a 30-year mortgage. At 6.5 % interest, however, you will pay only $568,861—a savings of $110,445.

6 Steps to Better Credit

1. Pay your bills on time. Creditors scrutinize your credit history. If you pay your bills on time, this reflects well on you. If you have a record of delinquent payments, you might want to consider credit counseling on how to better manage your finances.

2. Manage your debt. Your debt/income ratio - the percentage of your income that goes to paying off debt - is another gauge of your financial health. You can calculate this ratio by dividing your monthly minimum debt payments (excluding mortgage) by your monthly take-home income. If your debt payment absorbs:

- Less than 20% of your income, you are doing well

- Between 20% to 35%, consider reducing your overall debt

- More than 35% consider credit counseling or some type of aggressive debt-reduction strategy

3. Don't over-apply for credit. Limit the number of loan applications you submit. Each bid shows up as an inquiry in your credit report. Even if you're just comparison-shopping for the best rate, too many inquiries can be viewed as a desperate bid to obtain credit to get out of financial trouble.

4. Shred your documents. Be sure to destroy any piece of paper with Social Security or credit card numbers. Thieves often go through garbage retrieving people's identification so they can use this information to commit fraud.

5. Don't give information away. Never include your Social Security Number your checks, driver's license or health insurance card. Be extremely cautious how you use your Social Security Number, it is your key personal identification number that is a gateway to your personal identity. If required to provide this information, always ask if there is another option.

6. Check your credit reports on a regular basis. The only way to protect your name and credit is to be proactive. With the rise of identity theft cases, it is important to review your credit files, and to report any inaccuracies to the major credit reporting agencies.

Recognizing identity theft

There are several signs you may be a victim of fraud or identity theft:

- Not receiving bills or other mail you should be getting

- Receiving credit cards you didn't apply for

- Being denied credit for no reason

- Getting calls or letters about things you didn't buy

- Being served court papers or arrest warrants for things you know don't involve you

If one of the above has happened to you, it may simply be due to a clerical error. But never assume that it's just a mistake - always look into it to find out for sure.

What to do if you're a victim

-

Report the crime to the police immediately. Be sure to get a copy of your police report or case number

-

Immediately contact your credit card issuers. Get replacement cards with new account numbers Ask that old accounts be processed as “account closed at consumer's request” Follow up by writing a letter that summarizes your request to the credit card company

-

Place a fraud alert on your credit report Alert all 3 credit reporting bureaus Add a victim's statement to your report so that they must contact you to verify future credit applications

-

Correct any inaccurate information Request that inquiries you didn't initiate be removed from your report Make sure your Social Security Number, address, name, employer, and other important information are all correct Check to ensure all changes you requested have been made

-

File a complaint with the Federal Trade Commission: Consumer Response Center

600 Pennsylvania Ave, NW

Washington, DC 20580

Phone:

Toll-free: 1.877.FTC.HELP

TDD: 202.326.2502